Should Budget for ‘You Need a Budget’?

Best Software October 20, 2020 Michael Franco

Do you need You Need A Budget? While that might seem like a typo (or some kind of obscure Zen koan), we’re simply posing a question regarding the app called You Need A Budget, which we’ll call YNAB (like they do) from here on out to eliminate any confusion. YNAB does pretty much only one thing – help you create a budget and stick to it – and it does it really well. But is it worth its relatively steep annual fee? Let’s take a look.

After installing YNAB, you’ll be asked to connect your banking and credit accounts if you’d like. Doing so lets the app pull in all of your financial transactions which can then be assigned to different spending categories. If you aren’t comfortable handing over this information, you can also enter transactions manually, although the company uses some pretty serious encryption algorithms, so security doesn’t seem like an issue.

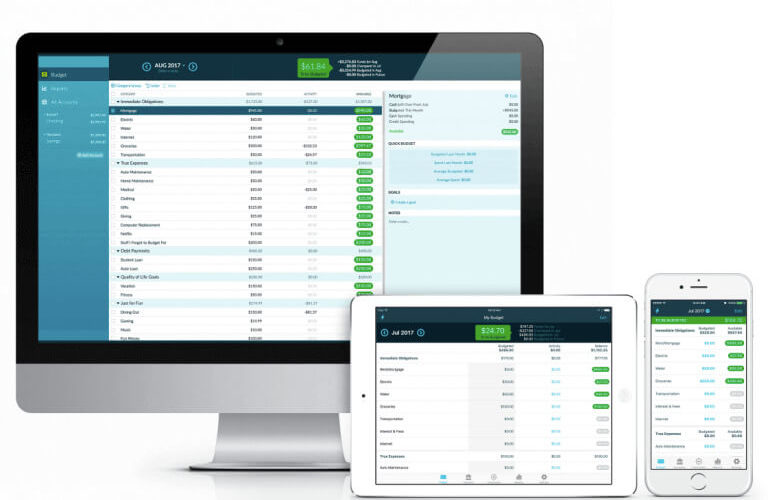

In either event, you can initially assign transactions to any of the app’s five categories: immediate obligations; true expenses; debt payments; quality of life goals; and just for fun. While YNAB says these categories can get you budgeting quickly and effectively, you also have the ability to change any of the category names, as well as add new ones.

Give Your Money a Job

Once your transactions are entered (or imported), YNAB will help guide you through their four-pronged approach to managing your money wisely. The main driver of the app is that it will require you to “Give Every Dollar A Job.” This means that for every deposit you make, you’ll need to assign every cent of it to one of your categories. The second principle the app puts to use is the idea that you should “Embrace Your Expenses,” meaning that not only should you cover regular monthly bills like utilities, but you should also save a bit each month to cover longer-term expenses like property taxes.

The third YNAB principle is “Roll With The Punches,” which basically means that you are allowed to move your money out of the categories you’ve put it in should unexpected expenses arise. If you need a car repair, for example, you might have to take some money away from your “life goals” or your “just for fun” categories. Finally, YNAB will guide to you “Age Your Money,” so that if you live paycheck to paycheck, you’ll be able to begin getting ahead of your expenses by having enough in your account to cover them before you get paid.

Beyond helping you apportion your money this way, YNAB also offers an extensive library of video lessons, has numerous question-and-answer opportunities, and will even pair you up with a personal coach to help you get started understanding and using the app.

So it’s pretty clear that YNAB has got the right tools and strategy to help you get a handle on your spending and help you work toward your financial goals. Its color-coded charts and graphs and easy-access interface (available for all major desktop and mobile platforms) also turns what is often seen as a dull task into more of an enjoyable game-like endeavor. But … is it worth its price tag?

The answer is: it depends.

Budget Wisely

If you purchase YNAB on a monthly basis, each payment will be $11.99. Sign up on an annual basis and you’ll save some cash, but you’ll need to shell out $84 per year. Clearly if you are someone who struggles with budgeting, saving, or getting a grip on your spending then you could certainly make up that cost by improving your financial picture using YNAB. According to the company, people that are new to budgeting save, on average, $600 in their first two months and $6000 after a year. If you were to see the same results, the app’s fee is a no-brainer.

But when you consider that other apps such as Mint also offer you a way to track, categorize and budget your spending for free, you might do best to try them out first.

Still, YNAB is more of a proactive app, helping you decide where you money is going to go before you spend it, rather than tracking it after the fact like Mint, so there is some value there.

Perhaps the best idea is to take advantage of YNAB’s 34-day free trial. This would let you get familiar with the program, learn a thing or two and find out if it really will help you save. No credit card is required for sign-up, so ending your trial is pretty easy, which is yet another reason why the software is easy to recommend.